Bitcoin Drops Below $86,000, but Is the Plunge Just Getting Started?

Original Article Title: "Bitcoin Price Drops Back to $10,000?! Bloomberg Expert Gives Most Pessimistic Prediction"

Original Article Author: Seed.eth, via Bitpush News

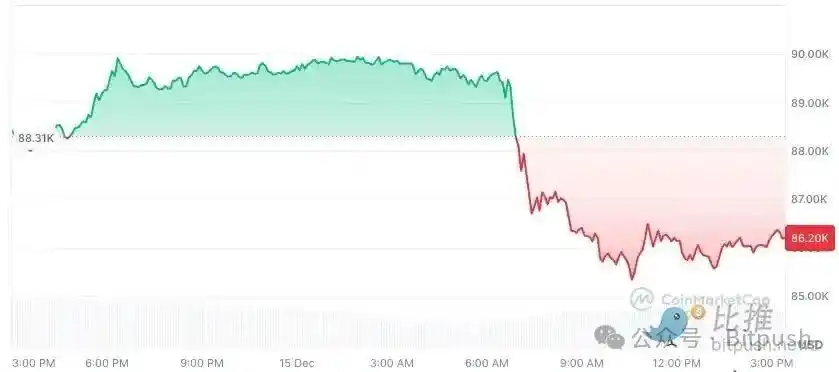

This past weekend, the crypto market did not see a sentiment recovery. After several days of narrow range trading, Bitcoin came under pressure on Sunday evening to Monday during the US stock market session, dropping below the $90,000 whole number level, with the intraday low briefly touching near $86,000. ETH dropped 3.4% to $2,980; BNB dropped 2.1%; XRP dropped 4%; SOL dropped 1.5% to around $126. Among the top ten cryptocurrencies by market cap, only TRX recorded a slight increase of less than 1%, while the rest were in a correction phase.

From a timing perspective, this was not an isolated correction. Since hitting a new all-time high in mid-October, Bitcoin has retraced more than 30%, and each rebound has appeared brief and hesitant. While ETF inflows have not shown systemic outflows, the marginal inflow has significantly slowed down, making it difficult to provide the market with the "sentiment cushion" as before. The crypto market is transitioning from unilateral optimism to a more complex and patience-testing phase.

Against this backdrop, Mike McGlone, Senior Commodity Strategist at Bloomberg Intelligence, released a new report placing Bitcoin's current trend into a broader macro and cyclical framework and made a highly unsettling judgment: Bitcoin is likely to return to $10,000 by 2026, which is not an alarmist statement, but one of the potential outcomes under a special "deflation" cycle.

The controversy surrounding this view is not just about the "low" number itself, but because McGlone does not view Bitcoin as an independent crypto asset, but rather reexamines it within the long-term coordinates of "global risk assets-liquidity-wealth reversion."

"Inflation After Deflation"? McGlone Focuses Not on Crypto, but on Cyclical Turning Points

To understand McGlone's judgment, the key is not how he views the crypto industry, but how he understands the macro environment of the next stage.

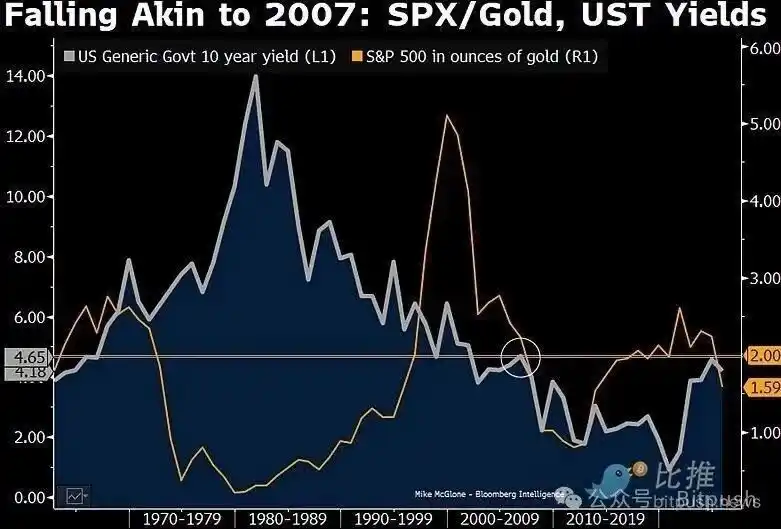

In his latest view, McGlone repeatedly emphasizes a concept: Inflation / Deflation Inflection. In his view, the global market is standing near such a key turning point. With major economies seeing peak inflation and growth momentum slowing down, asset pricing logic is transitioning from "inflation combat" to dealing with "inflation after deflation"—the stage where prices fall across the board after the inflation cycle ends. He wrote, "Bitcoin's downward trend may replicate the situation the stock market faced in 2007 in response to the Fed's policies."

This is not his first time issuing a bearish warning. As early as November last year, he predicted that Bitcoin would drop to the $50,000 mark.

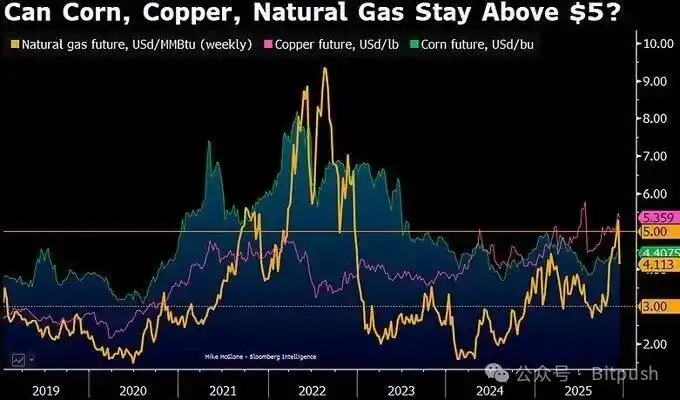

He pointed out that around 2026, commodity prices may fluctuate around a key axis—natural gas, corn, copper, and other core commodities' "inflation-deflation divide line" may settle near $5, and among these commodities, only assets like copper, which have genuine industrial demand support, may still be above this axis by the end of 2025.

McGlone noted: When liquidity recedes, the market will reevaluate "real demand" versus "financialization premium." In his framework, Bitcoin is not "digital gold" but an asset highly correlated to risk appetite and speculative cycles. When the inflation narrative recedes and macro liquidity tightens, Bitcoin often tends to reflect these changes earlier and more dramatically.

McGlone believes that his logic is not based on a single technical level but on the overlay of three long-term paths.

Firstly, it is mean reversion after extreme wealth creation. McGlone has long emphasized that Bitcoin is one of the most extreme wealth amplifiers in a global loose monetary environment over the past decade. When the growth rate of asset prices significantly outpaces economic activity and cash flow growth for an extended period, reversion tends to be not gentle but severe. Historically, whether it's the US stock market in 1929 or the tech bubble in 2000, a common feature at the top stage is that the market repeatedly searches for a "new paradigm" at highs, and the subsequent correction often far exceeds the most pessimistic expectations at that time.

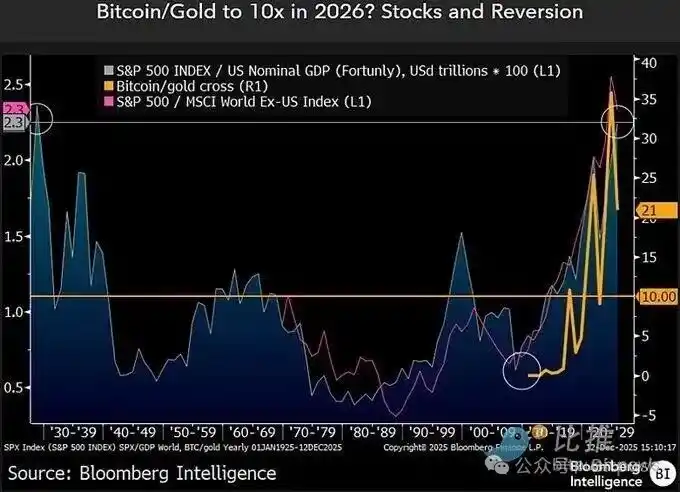

Secondly, it is the relative pricing relationship between Bitcoin and gold. McGlone places particular emphasis on the Bitcoin/gold ratio. This ratio was around 10x at the end of 2022, then rapidly expanded under the bull market drive, reaching over 30x at one point in 2025. However, this ratio has since fallen by about 40% this year, dropping to around 21x. In his view, if deflationary pressures persist and gold remains strong due to safe-haven demand, a further return of the ratio to historical ranges is not a radical assumption.

Thirdly, it is a systemic issue in the speculative asset supply environment. Although Bitcoin itself has a clear total supply limit, McGlone has repeatedly pointed out that what the market is truly trading is not the "uniqueness" of Bitcoin but the risk premium of the entire crypto ecosystem. When millions of tokens, projects, and narratives compete for the same slice of risk budget, during a deflationary cycle, the entire sector tends to be uniformly discounted, and Bitcoin finds it challenging to completely detach from this repricing process.

It should be noted that Mike McGlone is not a bull or bear spokesperson for the crypto market. As a senior commodity strategist at Bloomberg, he has long studied the cyclical relationship between crude oil, precious metals, agricultural products, interest rates, and risk assets. While his predictions may not always be pinpoint accurate, his value lies in: he often poses structural counter questions when market sentiment is most unanimous.

In his latest remarks, he also took the initiative to review his own "mistakes," including underestimating the timing of gold breaking $2,000 and deviations in his judgment of the U.S. bond yields and stock market rhythm. But in his view, these deviations have repeatedly confirmed one thing: the market is most prone to trend illusion before a cyclical turning point.

Other Voices: Divergence is Widening

Of course, McGlone's judgment is not market consensus. In fact, the attitudes of mainstream institutions are showing significant divergence.

Traditional financial institutions such as Standard Chartered have recently significantly lowered Bitcoin's medium to long-term price targets, reducing the 2025 target from around $200,000 to about $100,000, and also adjusting the 2026 speculative space from around $300,000 to about $150,000. In other words, institutions no longer assume that ETFs and corporate allocations will continue to provide marginal buying pressure in any price range.

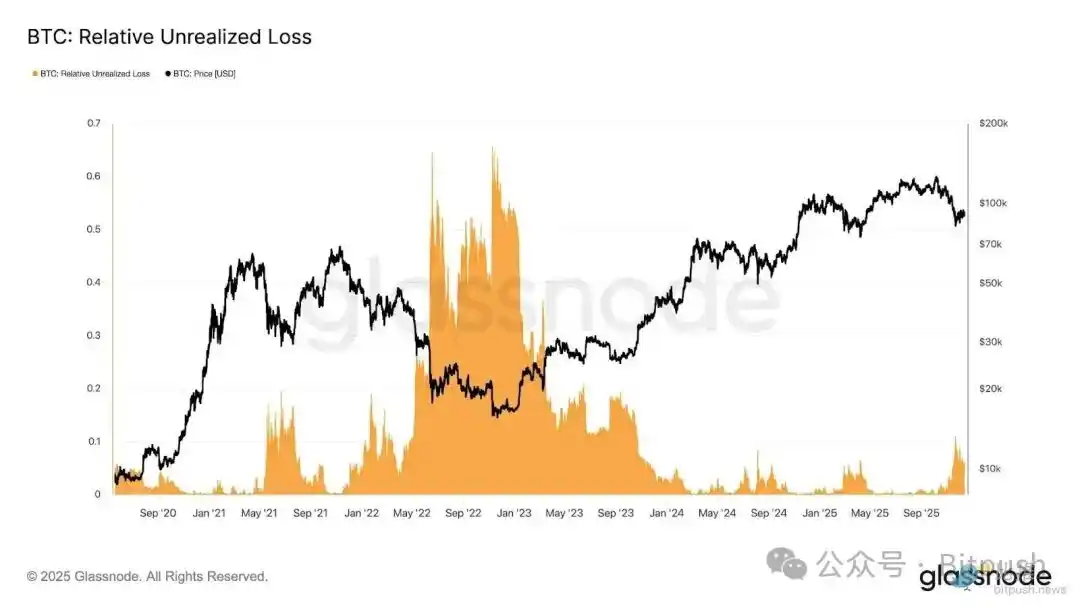

Research from Glassnode points out that Bitcoin's range-bound price action between $80,000 and $90,000 has put pressure on the market, with the intensity of this pressure akin to the trend at the end of January 2022. The current market's relative unrealized losses are approaching 10% of the market cap. Analysts further explain that such market dynamics reflect a state of "constrained liquidity, sensitive to macro shocks," but have not yet reached the level of typical bear market capitulation (panic selling).

10x Research, which leans more towards quantitative and structural research, has come to a more direct conclusion: they believe that Bitcoin has entered the early stages of a bear market, with on-chain indicators, fund flows, and market structure all indicating that the downward cycle has not yet run its course.

From a broader time perspective, the current uncertainty surrounding Bitcoin is no longer just an issue within the crypto market itself but is firmly embedded in the global macro cycle. The upcoming week is seen by many strategists as the most crucial macro window of the year-end—where the European Central Bank, Bank of England, and Bank of Japan will sequentially announce interest rate decisions, while the U.S. will see a series of delayed employment and inflation data releases, providing a belated "reality check" for the market.

The Federal Reserve sent an unusual signal at its December 10 interest rate meeting: not only did it cut rates by 25 basis points, but there were also rare dissenting votes, with Powell bluntly stating that job growth in recent months may have been overestimated. This week's intense macro data releases will reshape the market's core expectations for 2026—whether the Federal Reserve can continue to cut rates or has to hit the pause button for a longer period. For risk assets, this answer may be more important than any single asset's bull or bear debate.

You may also like

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

See “Buy Walls” & “Sell Walls” Instantly: WEEX Launches the Depth Chart for Smarter Trades

What Is Quick Trade on WEEX? 2 Ways WEEX Ends Chart-Panel Jumping

Morning News | Five major virtual asset platforms in South Korea have experienced 57 incidents of hacking and system failures in six years; Grayscale submits registration application for Canton ETF

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.