When the Prediction Market Shifts from 'Predicting' to 'Revealing the Truth': Delphi Officially Launches Prediction Market Coverage

For a long time, we have understood prediction markets as a very “rational” activity: people bet on the future based on public information, and market prices reflect consensus. However, over the past year, we have increasingly realized one thing: many prediction markets are not about “predicting the future” but about preemptively exposing those “results already known to a few.”

When an outcome is already certain but not yet public, the prediction market becomes an extremely brutal entity: it doesn't need leaks, anonymous tips, or even a single word. The flow of funds itself is the leak.

The Prediction Market is Changing the Nature of “Secrecy”:

Imagine a few scenarios:

· A hit TV show has finished filming, will the main character die?

· The selection process for a gaming award has mostly concluded, but the results are not yet announced

· An AI company is about to release crucial product or acquisition news

· Regulatory outcomes for a Crypto protocol, listing times, governance vote direction

In the traditional world, these are called “inside information.” But with the advent of prediction markets, they face a new challenge: as long as someone knows and can place a bet, it is challenging for the secret to avoid market capture. You don't need to know “who said what,” you just need to look at:

· Which options are disproportionately staked

· Which addresses are consistently betting at key times

· Which accounts repeatedly “correctly bet early” in similar events

This is not a conspiracy theory; it is a natural outcome of probability and incentives.

From “Content Reporting” to “Result Stress Testing”

This is also why we are starting to rethink the traditional news model. The previous content logic was: event occurs → a few know → report (publish) → public knows

However, the prediction market brings another path: event occurs → someone knows → someone bets → price starts to deviate → the world already “knew in advance”

There is even a more extreme path: event occurs → someone knows → someone bets → price starts to deviate → leading to a change in the event

Regarding this path, I can provide a classic example: at the end of Coinbase's (Nasdaq: COIN) Q3 2025 earnings call, CEO Brian Armstrong said a seemingly offhand remark:

“I got a bit sucked into a prediction market. I've been tracking a prediction market on what we would say on this earnings call... So, I have to get these words in before the call ends: Bitcoin, Ethereum, blockchain, staking, and Web3.”

These words were not random but were part of a prediction market where people bet on whether certain words would be mentioned during this earnings call. After Armstrong said this sentence, the relevant prediction markets settled immediately, and those who bet on the words being spoken correctly profited. Reportedly, there was around $80,000 in bets settled instantly on platforms like Kalshi and Polymarket.

In other words, without these bets, in another parallel universe, Brian Armstrong would have just gone through the earnings call process normally without intentionally saying these words. This is the "reality-distortion field" of prediction markets, where the act of betting itself has the power to alter reality. This phenomenon is common in sports betting, where outcomes are often manipulated due to insider control to favor the least bet-upon option. However, whether it's words spoken during a Coinbase earnings call or a football match, these events have minimal impact on our world. But with platforms like Polymarket and Kalshi growing, these topics will be closer to our everyday lives, and this "reality-distortion field" of prediction markets will increasingly affect our lives.

In the future, content will no longer be the starting point for information but a tool for validation and interpretation. In extreme cases, content can even change reality. This is what the BlockBeats prediction market report is doing: it's not a "prediction market guide" or a mere recounting of what happened on Polymarket and Kalshi.

What we truly care about are three things:

· Which events show odds changes that are not primarily driven by emotion or public information?

· Are there addresses consistently heavily betting on the "winning" outcome before results, with an unusually high historical accuracy rate?

· Do these behaviors point to some "known but undisclosed" facts?

We achieve this through analyzing:

· Topics and option odds in prediction markets

· Bettors' on-chain addresses and their associated behaviors

· Similar betting patterns in past events

to do one thing: treat the prediction market as a "covert stress-tester" rather than a mere opinion poll.

Currently, we are focusing on several key areas:

· Macro policy directions and geopolitics that can impact the capital markets

· AI Industry: Product release timings, acquisitions, key personnel changes

· Crypto Industry: Token Generation Events, regulations, governance outcomes, significant protocol changes

The Future of the Content Industry:

The real challenge of prediction markets is not accuracy, but rather that they are undermining a long-standing default order in the content industry and regulation: only information allowed to be spoken out will become "common knowledge." When everything is open for betting, secrets are will no longer be constrained by institutions, professional ethics, or news censorship but will instead continue to battle against the price discovery mechanism.

In a mild scenario, this means that the endings of TV series, award recipients, and business decisions will be known in advance by the market; while in an extreme scenario, it may even involve war and geopolitical conflicts: people can obtain "military intelligence" level information through bets made by soldiers on the war frontlines, directly influencing the course of the war. When the outcome is already known to a few, and the market allows betting around the outcome, the price itself may become an undeniable signal of reality.

The first time I felt awe towards the financial industry was when I read a story in college about Ray Dalio, the founder of Bridgewater Associates, who had helped McDonald's hedge chicken futures in his early years; in the United States, large restaurant chains almost always hedge their core raw materials synchronously with futures to withstand the drastic price fluctuations, ensuring that consumers can enjoy consistent quality and price-controlled McNuggets at any time. What made me awe-inspiring is not the later achievements of Dalio, but the first time I clearly realized: the original intention of the financial market's birth was never for trading itself, but to make the real world operate more stably and predictably.

The futures market helps people hedge commodity price risks, the stock market helps socially valuable enterprises finance and develop more efficiently; in this process, the participation of traders and speculators provides liquidity, farmers lock in future revenue in advance, and companies obtain a stable cost structure. Although market participants take what they need, the overall system is a long-term positive-sum game.

This also forces us to return to a more fundamental question: when such massive speculative liquidity as Polymarket already exists, is it possible to guide it towards more directions that truly generate positive EV? If an event, once it occurs, will have a significant impact on individuals' lives, assets, or decisions, do we have the opportunity to leverage the liquidity of prediction markets, and even evolve in the form of a combination of multiple markets into an "event insurance"-like product, similar to the "flight delay insurance" we have in our lives now, which, although cannot compensate for our flight delay losses, can provide people with some psychological comfort.

Prediction markets are not challenging a particular media outlet, but are questioning a larger issue: when the world begins to be bet on, who still has the power to decide "what can be known?" and "when can it be known?" We will continue to explore this path. In addition, the BlockBeats Prediction Market Analysis team has also been established, if you also love content and are curious about prediction markets, you are always welcome to join us. (Resumes can be sent to contact@theblockbeats.org or HR telegram @Jhy10vewh0 with the note "Prediction Market") We also welcome startup teams in the prediction market and AI-related fields to discuss with us. BlockBeats is committed to giving excellent startup teams maximum exposure to the best of its ability, contact email contact@theblockbeats.org

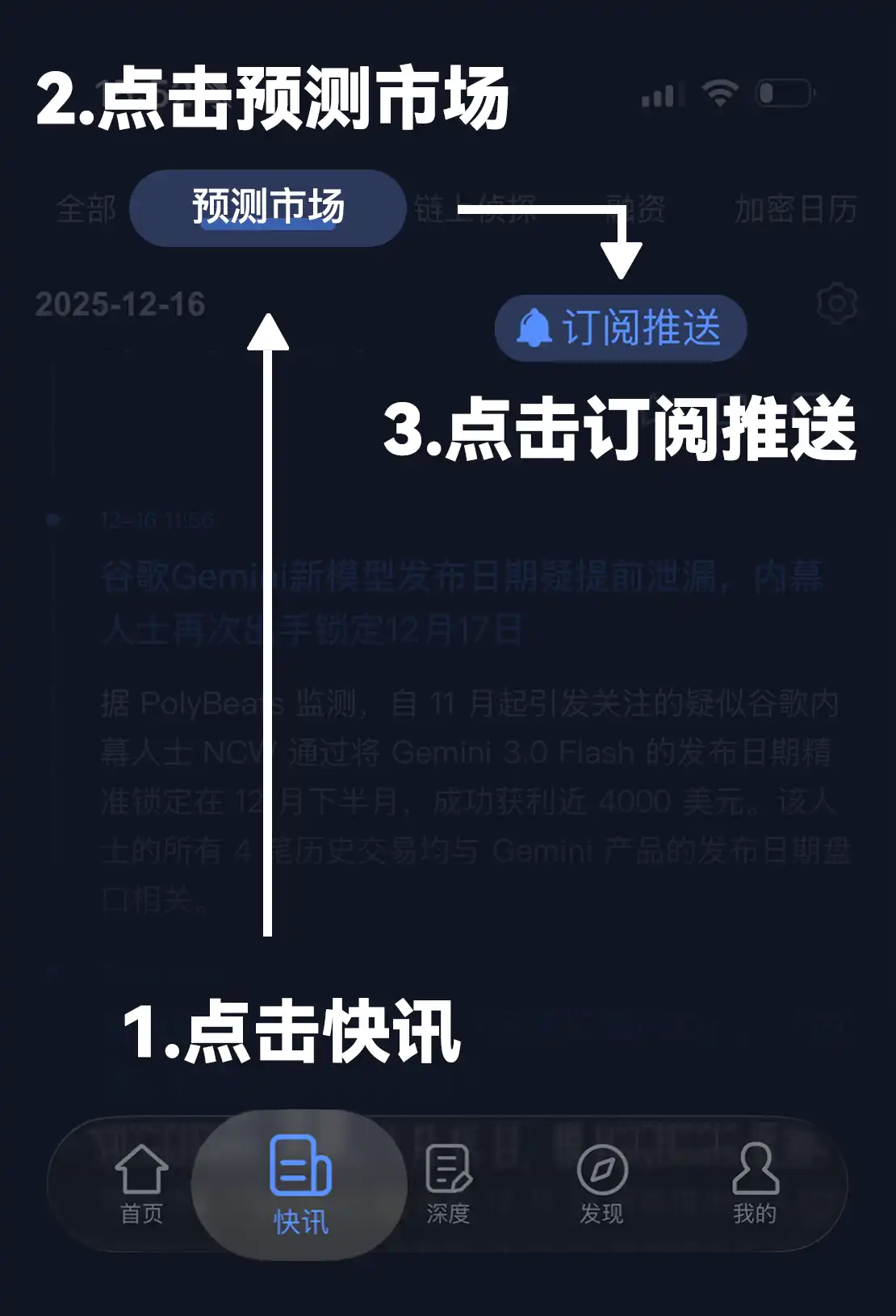

Finally, if you would like to receive timely updates on the prediction market news we uncover, you can subscribe on the Lydian APP. After subscribing, you will receive real-time prediction market news via in-app notifications. The specific steps are as shown in the image below (please make sure your APP is up to date).

You may also like

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

See “Buy Walls” & “Sell Walls” Instantly: WEEX Launches the Depth Chart for Smarter Trades

What Is Quick Trade on WEEX? 2 Ways WEEX Ends Chart-Panel Jumping

Morning News | Five major virtual asset platforms in South Korea have experienced 57 incidents of hacking and system failures in six years; Grayscale submits registration application for Canton ETF

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.