Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Why Should I Short SOL?

Original Author: The Giver

Original Translation: Ismay, BlockBeats

Editor's Note: This article provides an in-depth analysis of Solana's recent performance, discussing potential challenges from supply events, competitive pressures, complacency, among other perspectives, and predicts the future market trend. The author, through data and market phenomena, reveals Solana's potential concerns in terms of fund flows, ecosystem competition, and investor behavior, while also highlighting the changing trend of marginal buying and selling pressure in the market.

The following is the original content:

Here are some brief thoughts on Solana, mainly discussing why I believe Solana may underperform compared to other assets in December (I believe this trend has already started but will continue).

I opened a short position around ~$235-240 and believe this is the last excellent asymmetric opportunity of the year. However, it should be noted that I also hold short positions on other assets (such as Bitcoin, as the price gap between Saylor's buy-in price and the ETF is widening; also, I think if Ethereum falls, its downward trend may last even longer).

In summary, most of Solana's performance this year has not truly been tested, and its main driving force is running out (or in the process of running out).

Why will SOL underperform?

In my view, the real factors that have driven Solana to become the best-performing asset in the YTD among scalable assets this year include the following:

1. A more active and diversified ecosystem than its competitors, with fast transaction speeds;

2. The most powerful "casino" environment that has attracted many meme participants willing to use SOL as a unit of account;

3. Mid-year inflows — I believe many fund managers and large liquidity participants have been squeezed out due to the lack of ETH ETF heat, experiencing some form of "existence crisis" in future asset allocation.

Today, I believe the above three main driving forces have weakened and are highly vulnerable to shocks, with a significant amount of excess froth still needing to be trimmed. Here are my specific reasons:

As a speed- and diversity-focused leading L1, Solana faces a strong threat from HYPE and ETH/Base

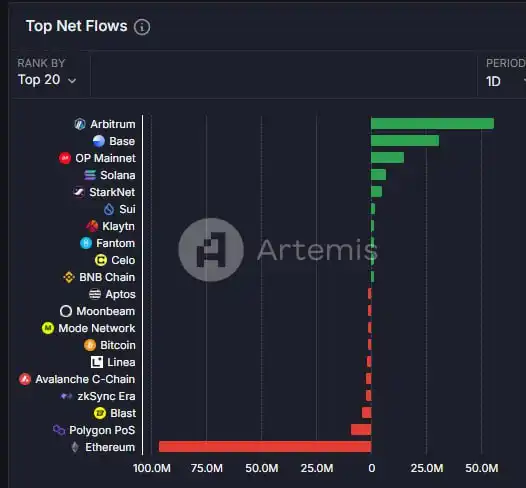

The rise of these threats has been unexpected and remains inadequately addressed.

The chart below shows Artemis traffic data, where you can choose to view it over a 1-week or 1-month period. This is the most significant instance this year of Solana's capital flow shifting to EVM, a shift that is reflected not only in traffic. We can also observe this in popular domain use cases, such as the meme coin sector in the AI domain—previously considered top-tier projects like GOAT, FARTCOIN, ZEREBRO, and AI16Z have all halved in valuation during this period, while the VIRTUAL and proxy ecosystems have flourished.

Furthermore, I believe Solana has not faced a true competitor in the L1 space for quite some time. While the HYPE is still in its early stages, its pursuit of democratizing ownership and the team's demonstrated strength are attractions that cannot be ignored in the short term.

Solana has yet to experience a true supply shock event by 2024

In contrast, other major assets have already undergone severe tests, such as Bitcoin's MTGOX incident and regulatory issues in Germany, as well as Ethereum's ETF launch. Solana has almost been unaffected in this regard, with only a brief fluctuation during the Jump sell-off earlier this summer, quickly brushed aside as ETH's larger retracement diverted attention.

The period of the last few months has been Solana's time to shine as a high beta asset to Bitcoin, capturing much of the capital flow from Ethereum (a trend that has gradually dissipated) while attracting attention far beyond lackluster, unappealing small-cap altcoins.

In the realm of liquid funds, for the 2024 fiscal year, GPs should have only two options for realizing cash distributions:

1. Distribute based on a percentage of realized gains;

2. Distribute based on a percentage of unrealized gains but subject to clawback adjustment based on the prior year's high watermark.

In either case, given Solana's outstanding performance last year, I believe fund managers would lean toward selling SOL, reasons for which may include:

a) As the best-performing asset of the year, it has seen a significant price increase;

b) It is believed that parts of the portfolio that have previously underperformed still have untapped upside potential and are more worthy of holding, while also observing other altcoins that have shown trend strength recently on the H1/H4/1 timeframes to capture gains.

Furthermore, this trend is also being driven by the hype around the Galaxy Auction (SOL cost basis at $80-100). Fund managers participating in the auction can profit in the following ways:

For example, selling one-third of the locked supply purchased near historical highs and then "reclaiming" these tokens in the first unlock event in March of next year to realize the price difference in nominal value.

The exit liquidity of the SOL ETF weakened due to the rise of established tokens and the potential impact of the XRP ETF

XRP's performance is being driven by two main factors:

a) It is considered the asset most likely to launch an ETF product after ETH, closely linked with Bitwise;

b) Rumors of the U.S. cryptocurrency capital gains tax dropping to 0%.

Considering XRP's track record (as one of the earliest crypto assets) and SEC Chair Gary Gensler's resignation, even if the probability of an XRP ETF launch remains on par with or slightly lower than SOL, it is undeniable that it is diverting market share that originally belonged entirely to SOL.

Complacency

Although this sentiment is difficult to quantify precisely, intuitively, I believe Solana's arrogance has reached a bottleneck, contrasting the situation from a few years ago — back then, ETH caught up with SOL head-on due to its superior position, and that position acted as an impenetrable moat.

Here are some typical examples:

1. "Network Expansion vs. L2"; DRIFT compared to HL, demonstrating an "incorruptible" attitude;

2. Many claim "no one would ever want to bridge from Solana to Base," despite clear counterexamples;

3. Some users who were staunch supporters of ETH surrendered completely a few weeks before ETH's 35% surge, with some suddenly strongly predicting that the target price for ETHSOL would plummet to very low levels (e.g., 0.027 ETHSOL).

Summary

In the next 30 days, I believe the attractiveness of Solana to marginal buyers is at its weakest point this year (ETF liquidity significantly lags behind ETH; the attention on altcoins is more diversified than before), while the selling pressure from marginal sellers is at its strongest (profit-taking; users who have made significant gains through memes or holding SOL choosing to sell to cash out and hedge).

Furthermore, as the bulls attempt to drive the price up, the funding cost remains high, with this upward movement being entirely leveraged-driven and reflected in recent (yet short-lived) ATH breaches.

You may also like

US AI Startup Goes All In on Chinese Mega-Model | Rewire News Morning Brief

Trump Lies Again: A "Five-Day Pause" Psyop, How Wall Street, Bitcoin, and Polymarket Insiders Synced Uposciogen

When a Token Becomes Labor, People Become the Interface

Ceasefire News Leaked Ahead of Time? Large Polymarket Bets on Outcome Before Trump's Tweet

BlackRock CEO's Annual Shareholder Letter: How is Wall Street Using AI to Keep Profiting from National Pension Funds?

Sun Valley Releases 2025 Financial Report: Bitcoin Mining Revenue Reaches $670 Million, Accelerating Transformation to AI Infrastructure Platform

On March 16, 2026, in Dallas, Texas, USA, CanGu Company (New York Stock Exchange code: CANG, hereinafter referred to as "CanGu" or the "Company") today announced its unaudited financial performance for the fourth quarter and full year ended December 31, 2025. As a btc-42">bitcoin mining enterprise relying on a globally operated layout and dedicated to building an integrated energy and AI computing power platform, CanGu is actively advancing its business transformation and infrastructure development.

• Financial Performance:

Total revenue for the full year 2025 was $688.1 million, with $179.5 million in the fourth quarter.

Bitcoin mining business revenue for the full year was $675.5 million, with $172.4 million in the fourth quarter.

Full-year adjusted EBITDA was $24.5 million, while the fourth quarter was -$156.3 million.

• Mining Operations and Costs:

A total of 6,594.6 bitcoins were mined throughout the year, averaging 18.07 bitcoins per day; of which 1,718.3 bitcoins were mined in the fourth quarter, averaging 18.68 bitcoins per day.

The average mining cost for the full year (excluding miner depreciation) was $79,707 per bitcoin, and for the fourth quarter, it was $84,552;

The all-in sustaining costs were $97,272 and $106,251 per bitcoin, respectively.

As of the end of December 2025, the company has cumulatively produced 7,528.4 bitcoins since entering the bitcoin mining business.

• Strategic Progress:

The company has completed the termination of the American Depositary Receipt (ADR) program and transitioned to a direct listing on the NYSE to enhance information transparency and align with its strategic direction, with a long-term goal of expanding its investor base.

CEO Paul Yu stated: "2025 marked the company's first full year as a bitcoin mining enterprise, characterized by rapid execution and structural reshaping. We completed a comprehensive adjustment of our asset system and established a globally distributed mining network. Additionally, the company introduced a new management team, further strengthening our capabilities and competitive advantage in the digital asset and energy infrastructure space. The completion of the NYSE direct listing and USD pricing also signifies our transformation into a global AI infrastructure company."

"As we enter 2026, the company will continue to optimize its balance sheet structure and enhance operational efficiency and cost resilience through adjustments to the miner portfolio. At the same time, we are advancing our strategic transformation into an AI infrastructure provider. Leveraging EcoHash, we will utilize our capabilities in scalable computing power and energy networks to provide cost-effective AI inference solutions. The relevant site transformations and product development are progressing simultaneously, and the company is well-positioned to sustain its execution in the new phase."

The company's Chief Financial Officer, Michael Zhang, stated: "By 2025, the company is expected to achieve significant revenue growth through its scaled mining operations. Despite recording a net loss of $452.8 million from ongoing operations, mainly due to one-time transformation costs and market-driven fair value adjustments, the company, from a financial perspective, will reduce its leverage, optimize its Bitcoin reserve strategy and liquidity management, introduce new capital to strengthen its financial position, and seize investment opportunities in high-potential areas such as AI infrastructure while navigating market volatility."

The total revenue for the fourth quarter was $1.795 billion. Of this, the Bitcoin mining business contributed $1.724 billion in revenue, generating 1,718.3 Bitcoins during the quarter. Revenue from the international automobile trading business was $4.8 million.

The total operating costs and expenses for the fourth quarter amounted to $4.56 billion, primarily attributed to expenses related to the Bitcoin mining business, as well as impairment of mining machines and fair value losses on Bitcoin collateral receivables.

This includes:

· Cost of Revenue (excluding depreciation): $1.553 billion

· Cost of Revenue (depreciation): $38.1 million

· Operating Expenses: $9.9 million (including related-party expenses of $1.1 million)

· Mining Machine Impairment Loss: $81.4 million

· Fair Value Loss on Bitcoin Collateral Receivables: $171.4 million

The operating loss for the fourth quarter was $276.6 million, a significant increase from a loss of $0.7 million in the same period of 2024, primarily due to the downward trend in Bitcoin prices.

The net loss from ongoing operations was $285 million, compared to a net profit of $2.4 million in the same period last year.

The adjusted EBITDA was -$156.3 million, compared to $2.4 million in the same period last year.

The total revenue for the full year was $6.881 billion. Of this, the revenue from the Bitcoin mining business was $6.755 billion, with a total output of 6,594.6 Bitcoins for the year. Revenue from the international automobile trading business was $9.8 million.

The total annual operating costs and expenses amount to $1.1 billion.

Specifically, they include:

· Revenue Cost (excluding depreciation): $543.3 million

· Revenue Cost (depreciation): $116.6 million

· Operating Expenses: $28.9 million (including related-party expenses of $1.1 million)

· Miner Impairment Loss: $338.3 million

· Bitcoin Collateral Receivable Fair Value Change Loss: $96.5 million

The full-year operating loss is $437.1 million. The continuing operations net loss is $452.8 million, while in 2024, there was a net profit of $4.8 million.

The 2025 non-GAAP adjusted net profit is $24.5 million (compared to $5.7 million in 2024). This measure does not include share-based compensation expenses; refer to "Use of Non-GAAP Financial Measures" for details.

As of December 31, 2025, the company's key assets and liabilities are as follows:

· Cash and Cash Equivalents: $41.2 million

· Bitcoin Collateral Receivable (Non-current, related party): $663.0 million

· Miner Net Value: $248.7 million

· Long-Term Debt (related party): $557.6 million

In February 2026, the company sold 4,451 bitcoins and repaid a portion of related-party long-term debt to reduce financial leverage and optimize the asset-liability structure.

As per the stock repurchase plan disclosed on March 13, 2025, as of December 31, 2025, the company had repurchased a total of 890,155 shares of Class A common stock for approximately $1.2 million.

The US AI Startup Is Loving China's Open Source Model

Three Weeks of the US-Iran War: Who's Making Money, Who's Paying the Bill?

Interpreting Polymarket's Major Update Last Night: Fee Expansion, Self-Regulation, and New Incentives

From Human Application to Intelligent Collaboration: How GOAT Network Builds the Next Generation Digital Economy

CZ Washington Dialogue: Crypto Entrepreneurs are Accelerating Their Return to the United States

Morning Report | Strategy increased its holdings by 1,031 bitcoins last week; Katana Blockchain acquires IDEX; NYSE completes rule change to eliminate trading limits on crypto ETF options

Electric Capital: Tracking 501 types of yield-generating RWA assets, we discovered these patterns

Those who are cut off by AI will not disappear; they will become the creators of the next round of the economy

Stablecoins reshaping cross-border payments in Asia? Strategic panorama and investment opportunity analysis

Zuckerberg is building an AI agent to help him as CEO

Bloomberg: Swiss Private Bank Old Guard Rifts, Is Bitcoin the Spark?

Zuckerberg is building an AI assistant to help him be CEO

US AI Startup Goes All In on Chinese Mega-Model | Rewire News Morning Brief

Trump Lies Again: A "Five-Day Pause" Psyop, How Wall Street, Bitcoin, and Polymarket Insiders Synced Uposciogen

When a Token Becomes Labor, People Become the Interface

Ceasefire News Leaked Ahead of Time? Large Polymarket Bets on Outcome Before Trump's Tweet

BlackRock CEO's Annual Shareholder Letter: How is Wall Street Using AI to Keep Profiting from National Pension Funds?

Sun Valley Releases 2025 Financial Report: Bitcoin Mining Revenue Reaches $670 Million, Accelerating Transformation to AI Infrastructure Platform

On March 16, 2026, in Dallas, Texas, USA, CanGu Company (New York Stock Exchange code: CANG, hereinafter referred to as "CanGu" or the "Company") today announced its unaudited financial performance for the fourth quarter and full year ended December 31, 2025. As a btc-42">bitcoin mining enterprise relying on a globally operated layout and dedicated to building an integrated energy and AI computing power platform, CanGu is actively advancing its business transformation and infrastructure development.

• Financial Performance:

Total revenue for the full year 2025 was $688.1 million, with $179.5 million in the fourth quarter.

Bitcoin mining business revenue for the full year was $675.5 million, with $172.4 million in the fourth quarter.

Full-year adjusted EBITDA was $24.5 million, while the fourth quarter was -$156.3 million.

• Mining Operations and Costs:

A total of 6,594.6 bitcoins were mined throughout the year, averaging 18.07 bitcoins per day; of which 1,718.3 bitcoins were mined in the fourth quarter, averaging 18.68 bitcoins per day.

The average mining cost for the full year (excluding miner depreciation) was $79,707 per bitcoin, and for the fourth quarter, it was $84,552;

The all-in sustaining costs were $97,272 and $106,251 per bitcoin, respectively.

As of the end of December 2025, the company has cumulatively produced 7,528.4 bitcoins since entering the bitcoin mining business.

• Strategic Progress:

The company has completed the termination of the American Depositary Receipt (ADR) program and transitioned to a direct listing on the NYSE to enhance information transparency and align with its strategic direction, with a long-term goal of expanding its investor base.

CEO Paul Yu stated: "2025 marked the company's first full year as a bitcoin mining enterprise, characterized by rapid execution and structural reshaping. We completed a comprehensive adjustment of our asset system and established a globally distributed mining network. Additionally, the company introduced a new management team, further strengthening our capabilities and competitive advantage in the digital asset and energy infrastructure space. The completion of the NYSE direct listing and USD pricing also signifies our transformation into a global AI infrastructure company."

"As we enter 2026, the company will continue to optimize its balance sheet structure and enhance operational efficiency and cost resilience through adjustments to the miner portfolio. At the same time, we are advancing our strategic transformation into an AI infrastructure provider. Leveraging EcoHash, we will utilize our capabilities in scalable computing power and energy networks to provide cost-effective AI inference solutions. The relevant site transformations and product development are progressing simultaneously, and the company is well-positioned to sustain its execution in the new phase."

The company's Chief Financial Officer, Michael Zhang, stated: "By 2025, the company is expected to achieve significant revenue growth through its scaled mining operations. Despite recording a net loss of $452.8 million from ongoing operations, mainly due to one-time transformation costs and market-driven fair value adjustments, the company, from a financial perspective, will reduce its leverage, optimize its Bitcoin reserve strategy and liquidity management, introduce new capital to strengthen its financial position, and seize investment opportunities in high-potential areas such as AI infrastructure while navigating market volatility."

The total revenue for the fourth quarter was $1.795 billion. Of this, the Bitcoin mining business contributed $1.724 billion in revenue, generating 1,718.3 Bitcoins during the quarter. Revenue from the international automobile trading business was $4.8 million.

The total operating costs and expenses for the fourth quarter amounted to $4.56 billion, primarily attributed to expenses related to the Bitcoin mining business, as well as impairment of mining machines and fair value losses on Bitcoin collateral receivables.

This includes:

· Cost of Revenue (excluding depreciation): $1.553 billion

· Cost of Revenue (depreciation): $38.1 million

· Operating Expenses: $9.9 million (including related-party expenses of $1.1 million)

· Mining Machine Impairment Loss: $81.4 million

· Fair Value Loss on Bitcoin Collateral Receivables: $171.4 million

The operating loss for the fourth quarter was $276.6 million, a significant increase from a loss of $0.7 million in the same period of 2024, primarily due to the downward trend in Bitcoin prices.

The net loss from ongoing operations was $285 million, compared to a net profit of $2.4 million in the same period last year.

The adjusted EBITDA was -$156.3 million, compared to $2.4 million in the same period last year.

The total revenue for the full year was $6.881 billion. Of this, the revenue from the Bitcoin mining business was $6.755 billion, with a total output of 6,594.6 Bitcoins for the year. Revenue from the international automobile trading business was $9.8 million.

The total annual operating costs and expenses amount to $1.1 billion.

Specifically, they include:

· Revenue Cost (excluding depreciation): $543.3 million

· Revenue Cost (depreciation): $116.6 million

· Operating Expenses: $28.9 million (including related-party expenses of $1.1 million)

· Miner Impairment Loss: $338.3 million

· Bitcoin Collateral Receivable Fair Value Change Loss: $96.5 million

The full-year operating loss is $437.1 million. The continuing operations net loss is $452.8 million, while in 2024, there was a net profit of $4.8 million.

The 2025 non-GAAP adjusted net profit is $24.5 million (compared to $5.7 million in 2024). This measure does not include share-based compensation expenses; refer to "Use of Non-GAAP Financial Measures" for details.

As of December 31, 2025, the company's key assets and liabilities are as follows:

· Cash and Cash Equivalents: $41.2 million

· Bitcoin Collateral Receivable (Non-current, related party): $663.0 million

· Miner Net Value: $248.7 million

· Long-Term Debt (related party): $557.6 million

In February 2026, the company sold 4,451 bitcoins and repaid a portion of related-party long-term debt to reduce financial leverage and optimize the asset-liability structure.

As per the stock repurchase plan disclosed on March 13, 2025, as of December 31, 2025, the company had repurchased a total of 890,155 shares of Class A common stock for approximately $1.2 million.